Conventional Refinance Rates, 2024 Limits and Guidelines

Conventional refinances are getting more and more popular with home values increasing across the country.

With a conventional refinance you can:

- Refinance a primary residence, second home or investment property

- Take out cash from your home’s equity

- Eliminate private mortgage insurance (PMI)

- Get rid of an FHA loan with Monthly mortgage insurance

- Reset or shorten the term of your loan

Conventional refinance rates are lower and have no upfront or monthly mortgage insurance fees if you have 20% equity or more in your home. You can also refinance into a conventional loan with less than 80% equity if you pay monthly mortgage insurance or use a lender paid mortgage insurance option.

What is a Conventional Loan Refinance?

Conventional mortgages are typically backed by government controlled agencies like Fannie Mae and Freddie Mac. These companies purchase loans that conform to certain standards that they require, which is why they are also called conforming loans, because they conform to those Fannie and Freddie Rules

Since these loans are backed by these agencies, banks can lend at lower rates on these Fannie Mae and Freddie Mac Eligible loans.

Conventional refinance rates are determined by a lot of different factors like credit score, loan-to-value, and what type of property you have. if you would like to find out what today’s conventional rate is based on your exact situation, you can find out here:

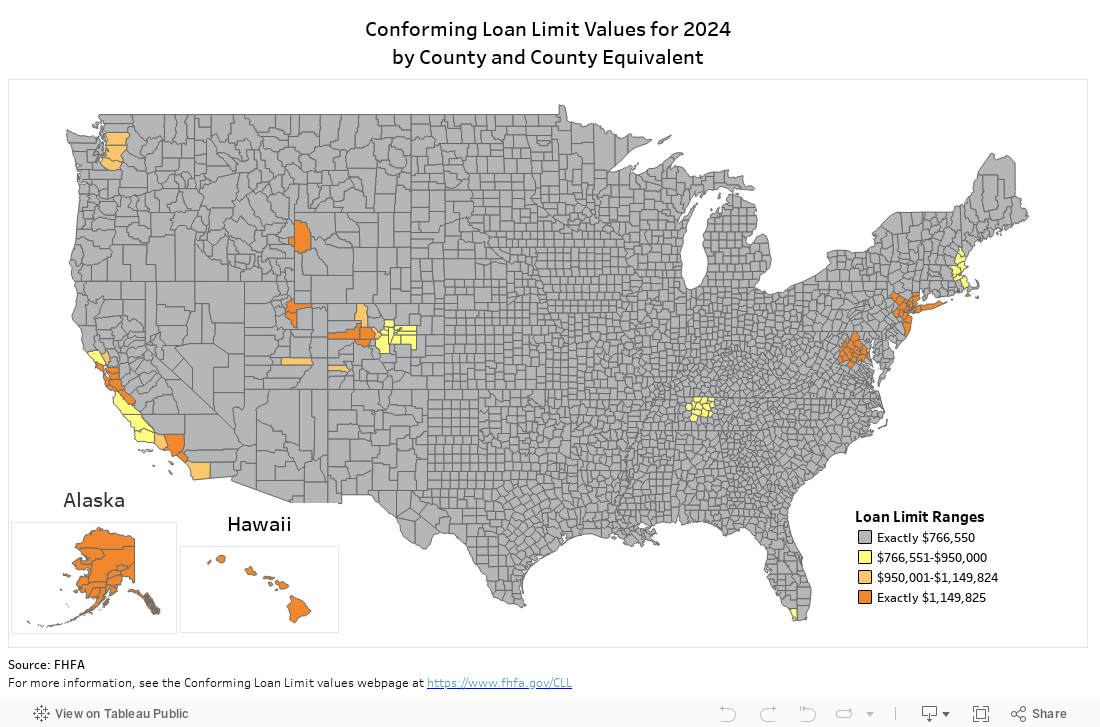

2024 Conventional Loan Limits

The standard loan limit in 2024 is $766,550 anywhere in the country, but Fannie Mae and Freddie Mac allow higher limits in high cost areas by county up to $1,089,300 in some counties.

Loan Limits by County

You should check and see what the limit is in your area before you look into getting a jumbo loan.

If you would like more information about loan limits in your specific area please contact one of our Conventional Mortgage experts